April 14, 2023: Global News Roundup

Price volatility, geopolitical risk, weather cloud outlook for global agricultural markets

This article was originally published on IPEwithSBB.org.

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global issues and events.

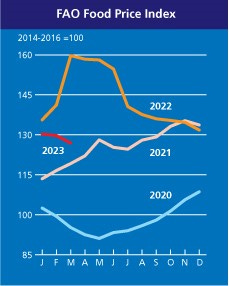

It’s spring in the Northern Hemisphere and autumn in the Southern Hemisphere, so there’s been a lot of planting and harvesting going on around the world over the past few weeks. Following a long year of shortages, supply chain shocks, and elevated prices, news on food and agriculture was somewhat hopeful, yet reflected the still-considerable uncertainty about global food supplies and prices moving forward. Let’s start with the UN Food and Agriculture Organization’s (FAO) food price index, which thankfully shows continued declines in world food prices off their peak last March 2022 when the impact of the Ukraine war hit commodities markets. Average prices have fallen roughly 35% since that time yet remain about 25% higher than the 2014-2016 base level.

(Image: FAO Food Price Index, April 2023, here).

FAO data released last week showed average world prices for cereal grains and vegetable oils declining since February (8.2% and 4.1%, respectively), which is good news especially for the world’s poorest households for whom grains and edible oils are dietary staples (prices per calorie for these staple foods are generally relatively low compared to calories from meat, dairy, and fresh produce). Given that 1 in 5 calories eaten on planet Earth is a calorie from rice, I was especially pleased to see in this month’s rice market report from the FAO that prices were down again in March (though still elevated over last year).

Other world news on cereal grains provided a mixed outlook. Heavy rains flattened wheat crops across India in recent weeks, and farmers lucky enough to still have a crop now have to harvest manually, which is much more costly and time consuming (when wheat is lying in the fields, flattened by heavy rains, it can’t be harvested by machine). It’s estimated that as much as 10% of India’s wheat crop has been damaged, with farmers in the northern state of Punjab reporting “blackened” (decaying) crops as well as exposed and shrunken grains that are now inedible. Punjabi wheat farmer Labh Singh told the India-based Tribune, “The grain has shrunk and there is no possibility of its recovery. Many farmers are hoping against hope, but the fact is we have lost our crop.” India is the world’s second largest producer of wheat. In the US, farmers planted their largest-ever acreage to wheat, but drought conditions are expected to limit yields such that there will likely be no overall production increases: “The U.S. Department of Agriculture on Monday pegged 28% of the U.S. winter wheat crop in good or excellent (GE) condition, the lowest for early April since 1996.” The US is among the world’s top 3 exporters of wheat, depending on the year.

(Image: “India wheat production”, AP Photo/Channi Anand, courtesy of Outlook India, here).

Moving on, FAO data shows meat prices up a bit over last month (less than 1%), and sugar prices up almost 2%. Interestingly, the FAO notes that declining oil prices have mitigated larger increases in global sugar prices, because Brazil (one of the world’s largest producers) has been able to use more of its sugarcane crop to produce sugar instead of using it to make ethanol: “The decline in international crude oil prices, encouraging a greater use of sugarcane to produce sugar in Brazil, coupled with the weakening of the Brazilian real against the United States dollar, contributed to limiting the month-on-month increase in world sugar prices.” (Depending on the year, Brazil diverts more than half of its sugarcane crop to fuel production; similarly, in recent years, the US has typically diverted 30-40% of its corn crop to ethanol production). Sugar prices hit a 7-year high on US futures exchanges this week and an 11-year high on the London markets, as investors priced in expectations of future shortages (heavy rain in Brazil) and growing demand.

Fertilizer prices, which were heavily impacted over the past year by the Ukraine war (alongside wheat, sunflower oil, among others), are also falling relative to last year’s peaks. (Last December, the EU agreed to ease up on fertilizer-related sanctions on Russia, citing the risk of global famine.) Mena FN reported this week that, according to a statement from the Brazilian ministry of agriculture and livestock, “fertilizer prices had a reduction of up to 70%, equalizing demand for 2023.” Recent fertilizer donations from the FAO, funded by the EU, to farmers in Sri Lanka nonetheless point to continuing cost pressures especially for smallholder farmers in debt-strapped, low-income economies.

Despite the recent respite from the global food storm, agricultural commodities markets remain highly volatile, and the future outlook is uncertain. Unsurprisingly, a major factor that keeps popping up is elevated geopolitical risk. For example, concerns about the increasingly hostile international landscape figured prominently in the CME’s discussion of price volatility from November, including concerns about wheat markets in connection with the Black Sea Grain Initiative, a deal struck last year between Russia and Ukraine to allow grain-bearing ships to traverse the sea safely, bringing Ukrainian wheat to the global market.

News this week indicated good reason for concern on this front, with Russia announcing yesterday that they will not extend the Black Sea grain deal beyond May 18 unless “the West removed a series of obstacles to the export of Russian grain and fertilizer”. Relatedly, US agribusiness giant Cargill announced two weeks ago that it was “stepping back” further from the Russian grain market and would no longer be elevating Russian wheat at its export terminal (“elevating” = moving grain onto ships for export). “The move stoked concerns about global grain supplies disrupted by the 13-month-old war in the Black Sea breadbasket region, lifting benchmark wheat futures prices to multi-week highs,” according to Reuters.

The World Bank’s April 10 food security update emphasized continued food price problems, noting “high inflation in almost all low- and middle-income countries, with inflation levels above 5% in 82.4% of low-income countries, 93% of lower-middle-income countries, and 89.0% of upper-middle-income countries and many experiencing double-digit inflation. In addition, about 87.7% of high-income countries are experiencing high food price inflation. The countries affected most are in Africa, North America, Latin America, South Asia, Europe, and Central Asia.” Speaking to geopolitical risks, the report also cites shipping bottlenecks in the Black Sea related to the Ukraine war as a major issue, noting that global wheat supplies remain tight. Last, the report notes the growing incidence of trade protectionism, as countries moved to ban or otherwise limit food exports, as well as the fact that roughly 200 million people in 45 countries are currently facing acute food insecurity.

Also of interest, the UN Committee on Trade and Development’s (UNCTAD) April report on global trends and prospects noted that global growth “decelerated” in late 2022, and that “the world economy has begun 2023 in a more fragile state than the optimistic accounts were suggesting”. The report goes on to discuss the dangers of speculation in agricultural markets, the power of large multinational agribusinesses over the food system (especially the ABCDs, which control the global grain trade, among other critical markets), and the ongoing global food crisis: “Partly due to the recent breakdown in commodity supply chains, their control over the production chain and price volatility, these companies registered up to a threefold increase in profits in 2021 (Public Eye, 2023). In the context of rising prices and heightened food insecurity around the world, the food trading sector warrants closer attention.” It is curious to me that UNCTAD is commenting on the role of monopolistic agricultural trading companies, a brand of criticism that I’ve seen only recently coming from this international agency. In regard to political risk, it makes me think that new regulations on speculation in commodity markets may be forthcoming. (See also my 2012 book and much shorter 2013 article for more detail on the relationship between speculative finance and food and agricultural production and trade.)

Things I’m keeping an eye on:

1. Taiwan: I noted last week that China had deployed fighter jets and naval vessels toward Taiwan in advance of President Tsai’s visit to the US. Over the weekend, China ended up conducting a full blown military exercise, encircling the island and practicing strikes and other maneuvers. Yesterday, the Taipei Times reported that the US is preparing a $19.5 billion arms shipment to Taiwan. The news was delivered by US Senator John Hoeven, who is visiting the island this week.

2. The USD: This story just won’t quit, and the global mood on the dollar is rapidly shifting. I reported last week on the rapidly declining support for the US dollar among the BRICS, prospective BRICS members like Saudi Arabia and Iran, and even among European countries like France and Germany. Right after I published last week’s post discussing dwindling European support for Taiwan’s defense and the US dollar, French President Macron made some controversial remarks about the dollar’s dominance and also indicated that France may decide to be more neutral if the Taiwan issue escalates further (maybe Macron reads my Substack…). And, Brazilian President Lula da Silva travelled to China this week to meet with President Xi about future economic and political cooperation. Lula’s comments during the trip addressed the dollar’s global dominance in some of the strongest and boldest terms I’ve seen yet from a world leader on this issue. The Financial Times reported on his comments yesterday as follows:

“Every night I ask myself why all countries have to base their trade on the dollar,” Lula said in an impassioned speech at the New Development Bank in Shanghai, known as the “Brics bank”.

“Why can’t we do trade based on our own currencies?” he added, drawing loud applause from the audience of Brazilian and Chinese dignitaries. “Who was it that decided that the dollar was the currency after the disappearance of the gold standard?”