December 1, 2023: Global News Roundup—Year in Review

December 1, 2023: Global News Roundup—Year in Review

Needful things—Commodities and the international balance of power

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global issues and events.

Good morning! This is the first of a short series of year-end reviews I’ll be sharing over the next month or so. Each review covers international news, as usual, and also takes stock of a major trend in global politics and economy during 2023 that I see as especially significant moving forward into 2024 and beyond.

Today’s post is dedicated to thinking about the growing power of non-Western commodities exporters. Historically, many countries that relied on the production and export of raw materials occupied a low rung in the global economic hierarchy, a persistent and ugly remnant of the older, colonial division of labor, one that positioned colonized territories and peoples across Latin America, Africa, the Middle East, and Asia as suppliers of cheap raw materials to industrial empires in North America and Europe. In the past, being a raw materials producer consigned entire communities and nations to poverty, marginalization, and political impotence. This old system is giving way to a new one in which former colonies and other “economic backwaters”—this 2020 article from The Diplomat refers to China in these terms—are increasingly wealthy, powerful, and influential players on the global stage.

The growing power of commodities producers and exporters is intertwined with a variety of dynamics I’ve covered extensively over the past year, including mounting backlash to Western dominance and neocolonial power, the rise of the BRICS+, the decline of the US dollar, the Ukraine war, inflationary pressures in energy and food markets, and “green” energy transitions that have increased demand for a variety of raw materials. This context is elevating global competition for basic commodities and, to varying degrees, empowering the countries where they are grown, raised, extracted, and mined.

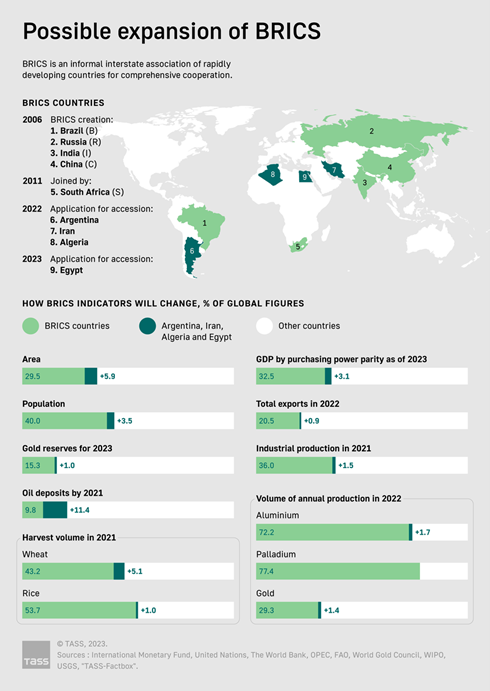

To start, it is worth noting that Brazil, Russia, India, China, and South Africa (BRICS)—which now account for a greater share of global GDP than the G7—specifically understand their growing power and influence in commodity-based terms. Russian state news outlet TASS published the infographic below back in June, in advance of the August BRICS summit which resulted in approved membership applications for Saudi Arabia, the UAE, Ethiopia, Egypt, Argentina, and Iran. The infographic shows the combined economic weight of BRICS members plus 4 other countries that were prospective members at the time of publication, together accounting for about 30% of global gold production, almost 50% of global wheat production, 55% of global rice production, and 80% of global aluminum production. The BRICS are, quite literally, measuring their power using raw materials production as a yardstick.

(Image: “Possible Expansion of BRICS”, TASS, June 15, 2023, here.)

Last week, Pakistan announced that it had officially applied for BRICS membership, with Foreign Office spokesperson Mumtaz Zahra Baloch stating that “Pakistan can play an important role in furthering international cooperation and revitalizing inclusive multilateralism.” (“Inclusive multilateralism” refers to a world system in which there is no single dominant superpower and, instead, many countries share more equally and peaceably in global wealth and power.)

Pakistan is a major exporter of cotton and copper, among other critical raw material and, this week, a major mining company from the United Arab Emirates (UAE), National Trust, announced a partnership with a Pakistani firm to “mine, acquire, and process aluminum ore in Punjab and potentially export it to the Middle East”. Pakistan’s Express Tribune noted that, “Apart from bauxite, Pakistan has reserves of barite, calcium fluoride (fluorspar), copper, phosphate, etc., and [National Trust] has also shown interest in procuring these minerals.”

In contrast to groupings like the G7, which collects 20th century (mostly Western) industrial and financial powers, the BRICS+ (original 5 members plus new members) is distinguished as a group of major commodities exporters, exhibiting varying degrees of industrial and financial sophistication, working with other commodity exporters to produce, extract, mine, refine, and trade critical raw materials.

To this point, last week the government of Mali announced a new partnership with Russia to “build a gold refinery in the capital Bamako, one of a slew of deals between the two countries as Russia seeks to extend its regional influence”. According to Reuters, the new Mali-Russia commodity partnership is one of many mineral and energy projects slated for development in the wake of a 2021 coup in which French military forces were expelled from the west African nation:

The deal is the latest sign of Russia's deepening interests in Mali, one of Africa's largest gold producers, just as Western influence there wanes.

Russia's state nuclear energy company Rosatom signed a deal with Mali in October to explore for minerals and produce nuclear energy. Sanou said he had also signed a deal with a Russian firm to build a 200- to 300-megawatt solar power plant by mid-2025.

Mali's military, which took power in a 2021 coup, last year kicked out troops from former colonial power France, who were fighting Islamist militants, and teamed up with the Russian military contractor Wagner Group, which has operations across Africa, including lucrative mining deals.

Recall also that the July 2023 military coup in Niger, another former French colony, revolved in part around France’s historic role in the country, including its military presence and extensive investments in and control over Niger’s uranium and gold resources. Following the coup, the new government, which is backed by Russia, flexed its commodity exporter muscles and suspended exports of uranium to France.

As suggested by Russia’s foray into mining in Mali, the frantic global pace of gold mining, refining, and stockpiling has been a central piece of the geopolitical puzzle over the past year. In response to US sanctions on Ukraine, rising inflation, and growing financial instability in the West (including the decline of the US dollar), foreign central banks have been rapidly stockpiling gold, including moves to repatriate gold stocks held in Western vaults. A report from Canadian gold trading firm Kitco in July noted that, “A substantial percentage of central banks are concerned about the precedent set by the U.S. freezing of Russian reserves, with the majority (58%) agreeing that the event has made gold more attractive” (see also this piece on repatriation of gold by non-Western countries).

Rising gold demand and prices means growing power and influence for major producers and stockpilers, including the BRICS. In China’s case, gold production and stockpiling takes on even greater significance as the US dollar’s strength wanes, with many speculating that China today is initiating some kind of gold-based oil trading mechanism to support de-dollarization and the internationalization of the Chinese currency, the yuan (a.k.a. the renminbi).

Writing for the French multinational banking giant BNP Paribas back in June, analyst Chi Lo noted,

Gold, however, is a key factor in the further development of a petro-yuan system. A gold-backed petro-yuan does not require full renminbi convertibility to function, so it allows China to simultaneously retain control of its capital account and boost the internationalization of the renminbi…Making the renminbi convertible into gold effectively turns the currency into a global investable asset for foreign renminbi owners, boosting their confidence in and demand for the Chinese currency.

Indeed, China was the world’s largest producer and consumer of gold in 2022 and appears to be leveraging its existing stocks and relations with other gold producers to undermine US financial dominance. The SCMP reported in mid-November that Hong Kong, a gateway for gold inflows to mainland China, had replaced Dubai as the biggest hub for trade in gold bullion of Russian origin. Further, in an unprecedented market development, in recent months international gold markets have bifurcated, with the price of physical gold traded on China’s Shanghai Gold Exchange (SGE) posting premiums over gold futures prices (“paper” gold) on US and European exchanges: “At the same time, gold premiums on the Shanghai Gold Exchange vs. prices in Comex gold futures have hit record highs. The price premiums in China have started to attract significant attention on social media, with many analysts commenting on this unprecedented environment…[Some analysts] have speculated that the higher SGE premiums are due to China's push to strengthen the yuan's international credibility and promote the petro-yuan.”

China has further leveraged its dominance in rare-earth mineral production to undercut Western economic prowess, including controls on exports of germanium and gallium to the US back in July. China implemented new export controls on graphite-based materials this week, now requiring permits for exporting a series of 9 products used in electric vehicle batteries.

In similar news, Mena FN reported that Western governments are wary of Chinese dominance in rare earths and their own vulnerability in this context, and have been meeting with Latin American governments and companies (including in Argentina) to secure supplies of lithium, a rare earth mineral essential for manufacturing lithium ion batteries and fuel cells.

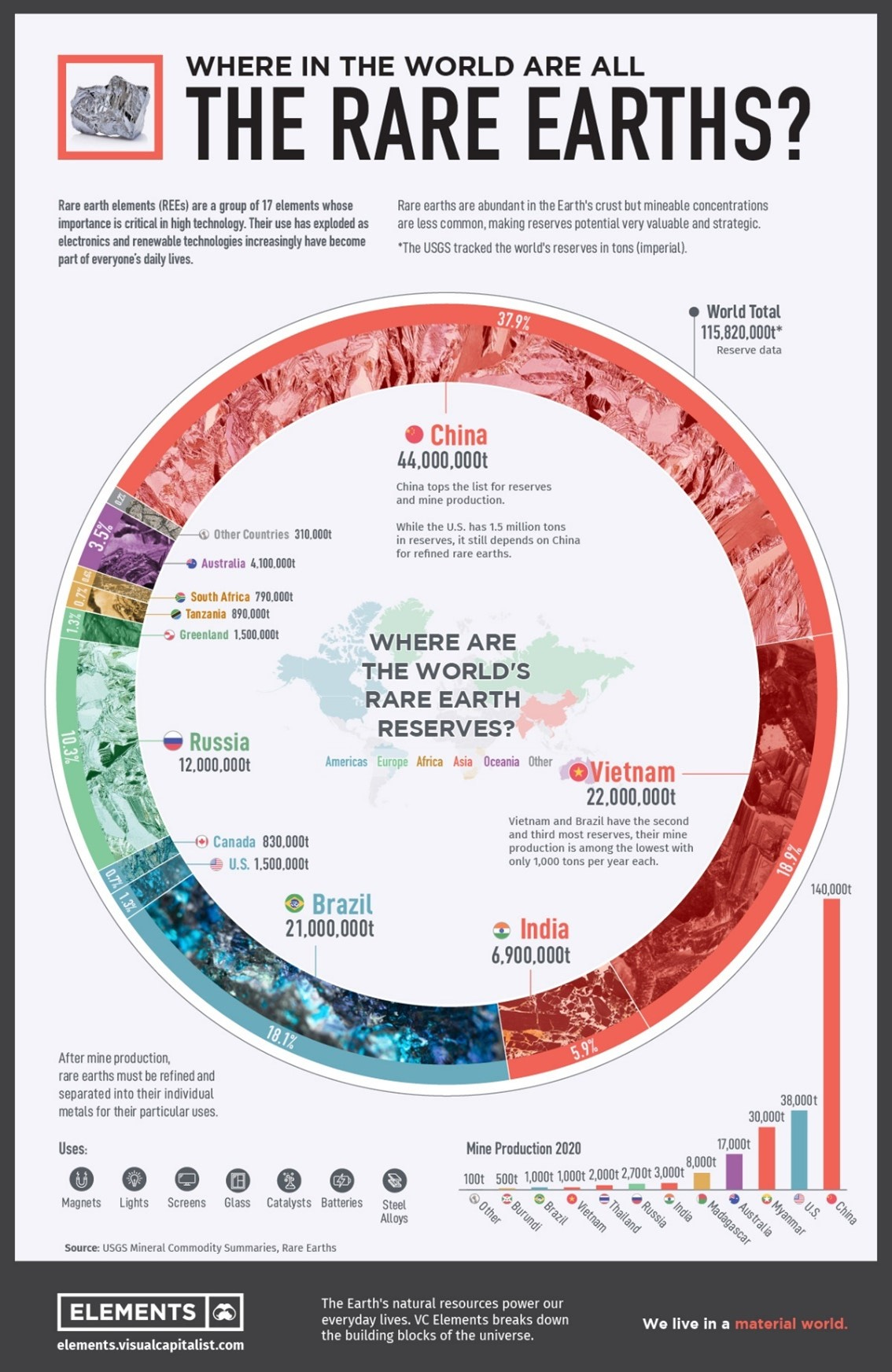

The image below depicts the geographic distribution of rare earth mineral deposits. Note how dominant the BRICS nations China, India, Russia, and Brazil are in this context.

(Image: “Where in the World are All the Rare Earths?” From Visual Capitalist, 11/23/2021, here.)

Things I’m keeping an eye on:

1. Copper politics: The Supreme Court of Panama directed Canadian mining company First Quantum to cease work at the Cobre Panama mine this week, following its decision that the mining contract for the operation was unconstitutional. “The top court’s ruling capped six weeks of protests and official announcements over a contract that gave First Quantum 20 years of mining rights over the giant copper asset, with an option to extend the deal for another 20 years in return for $375 million in annual revenue to Central American nation”, reported the Canadian Mining Journal. Copper prices rose and First Quantum process fell on the news.

Calling copper a “vital metal”, Canada’s Globe and Mail argued that, “The Russian invasion of Ukraine highlighted the folly of relying on potential adversaries for your energy security. It led to the realization among the West’s political class that the production of most energy-transition metals is concentrated in a handful of countries, many of them politically unstable, before being refined in China. The supply chain for clean electricity is a tightrope.” The article further discusses the likelihood of a “structural deficit in global copper supplies”, owing to protests and other supply disruptions in Peru and China, amounting to about 10 million metric tons by 2035 and likely undermining efforts to achieve “net zero”.

2. OPEC: The Organization of Petroleum Exporting Countries, which has been using its weight in energy markets to frustrate US and European interests over the past year or so (see, e.g., here and here), is adding a new member. This week’s OPEC meeting resulted in an invitation to Brazil to join, and Brazil’s energy minister said they hope to officially accede in January. Note the growing overlap between OPEC and BRICS members, demonstrating how cooperation among non-Western commodities exporters is ratcheting up (OPEC members UAE, Iran, and Saudi Arabia are set to join the BRICS early next year).

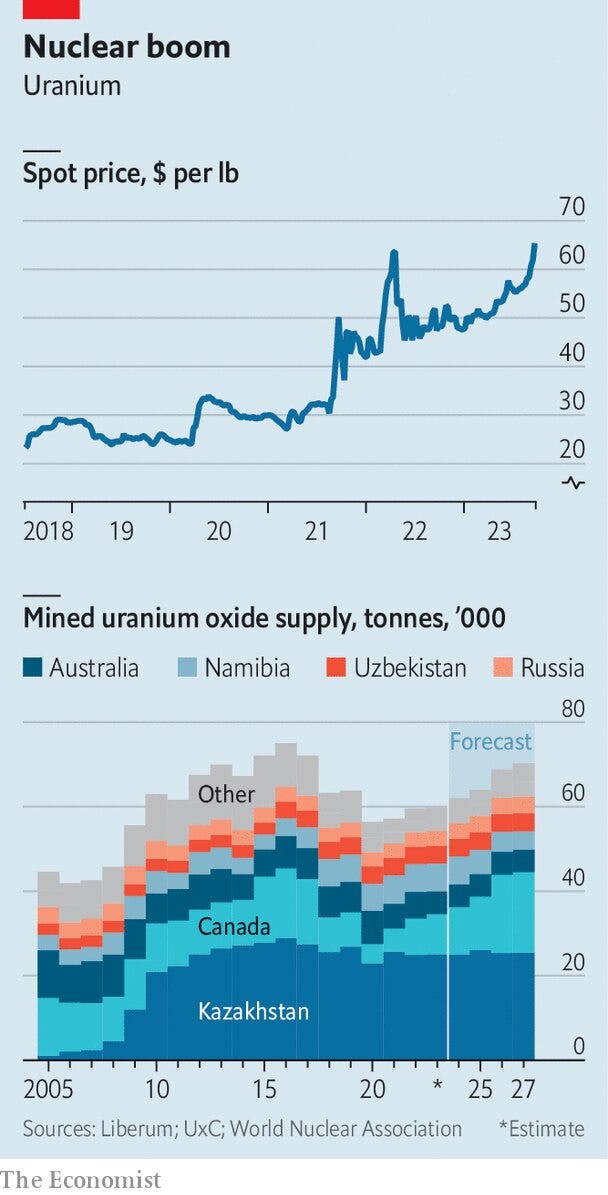

3. Uranium politics: Prices for uranium have reached record highs in recent weeks as demand outpaces global supplies. With the Ukraine war and energy price inflation reigniting global interest in nuclear energy, major European suppliers are running low on inventory and at least one is “sold out” until 2027. The chart below from The Economist shows the rising price of uranium in the top frame, and major global uranium producers in the bottom one. Notice the major share held by Kazakhstan, a Russian ally and member of the Eastern Economic Union (an economic union with Russia, Belarus, Kyrgyzstan, and Armenia), and member of the Chinese-led Shanghai Cooperation Organization (SCO). Russia also accounts for a large share, as does Namibia (The largest mine in Namibia, the Rossing mine, was recently sold to the China National Uranium Company).

(Image: “Nuclear boom”, from The Economist via LiveMint, 11/24/2023, here.)