June 24, 2022: Global News Roundup

Skyrocketing commodities prices usher in food, energy, debt crises

Obvious signs of cascading crises in food, energy, and finance, spawned by months of rising commodities prices, are coming in quickly this week, with indicators pointing to a very difficult remainder of the year, with a strong probability that food and fuel prices will remain relatively high even into 2023-2024 (see also the World Bank’s assessment from April here).

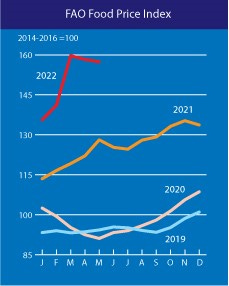

While in June global food prices are, on average, down slightly from recent highs, the UN Food and Agriculture Organization (FAO) Food Price Index, below, confirms, global food price increases of more than 30% since June of last year and more than 65% since June 2020, shortly after the pandemic began.

(Source: FAO Food Price Index, https://www.fao.org/worldfoodsituation/foodpricesindex/en/, accessed 06/22/2022.)

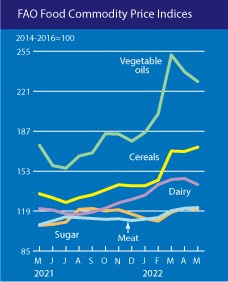

(Source: FAO Food Commodity Price Index, https://www.fao.org/worldfoodsituation/foodpricesindex/en/, accessed 06/22/2022.)

As you can see in the FAO Food Commodity Index above, the sharpest increases are for vegetable oils, up more than 75% just since December, and cereal grains, up about 35% over the past year. These figures are especially worrisome given that basic fats and grains are the most important sources of calories for the world’s poor.

UN World Food Program (WFP) chief David Beasley warned this week of “frightening” shortages and an “unprecedented” food crisis on the horizon. The UN Conference on Trade and Development (UNCTAD) likewise noted earlier this month that “The war in Ukraine has trapped the people of the world between a rock and a hard place. The rock is the severe price shocks in food, energy and fertilizer markets due to the war, given the centrality of both the Russian Federation and Ukraine in these markets. The hard place is the extremely fragile context in which this crisis arrived; a world facing the cascading crises of the COVID-19 pandemic and climate change.”

In Ethiopia, farmers are struggling to access fertilizer and seeds, and “are in serious danger of losing the main planting season (June-August) if they do not receive urgent support from the international community to sow their fields, which would further deteriorate the already serious food security situation in the region.” In Sudan, “a record 11.7 million people, almost a quarter of the country's population, are projected to be facing acute hunger at the height of the lean season in September— an increase by nearly 2 million people compared with the same period last year.” In Afghanistan, where the US has tried to limit the Taliban’s access to resources by blocking access to external finance (including foreign aid), rising food prices are outpacing the capacity of residents and policymakers to cope: “The Taliban regime is not in a position where it can feed the Afghan people. A large number of Afghans are facing a hunger crisis for the first time. Hunger is evident in every town, village and street across the country. Long queues outside bread shops and scuffles over food in different parts of the country are now a daily sight.”

Moreover, rising food and energy prices appear to be setting off a string of financial crises, not unlike the 1980s debt crisis in which more than 40 governments across the developing world defaulted on their debts in rapid succession. (I really like this book by Susan George and this book by Noreena Hertz as introductions to the 1980s debt crisis and the “lost decade” that followed across the global South). When commodity prices rise, countries that rely on imported food and fuel may, in addition to widespread hunger and civil unrest, also face economic and financial problems related to trade deficits and currency collapse (because import costs rise so quickly in relation to export earnings).

In the Philippines, rising fuel prices are contributing to soaring import costs and a rapidly depreciating national currency, paralleling some of the dynamics that preceded the “complete collapse” of Sri Lanka’s economy over the past several months. Meanwhile, Pakistan was in talks with the International Monetary Fund (IMF) this week to revive its bailout loan program as the country’s economy “teeters on the brink of a financial crisis”, with rising food and fuel costs quickly eating up foreign exchange reserves. China extended a US$2.3 billion loan to beleaguered Pakistan this week, among other global lenders stepping in to provide emergency credit. The business community in Kenya is reporting that dollar reserves are running low, though, as in the Philippines, the government is disputing these claims: “It is the demand [for dollars] that has risen significantly because the costs of goods globally have risen dramatically”, says Kenya Bankers Association Chairman John Gachora.

Even many of the world’s richest countries are struggling to manage shortages and rising costs. In Germany, which imports more than half of its gas and coal from Russia, “Economy Minister Robert Habeck triggered the second stage of the country's three-phase gas emergency plan on Thursday, moving Europe's biggest economy to the "alarm" level following steep cuts in supplies from Russia.” In France, President Macron’s party lost its parliamentary majority, with pundits attributing the result in part to the impact of turbulence in food and energy markets on voters. Italian Foreign Minister Luigi Di Maio warned this week that rising commodity prices threaten to destabilize the region, “Tensions in energy and basic commodities markets and the worsening of food insecurity that the conflict in Ukraine is generating at the global level constitute a further threat - first and foremost to the stability and development of the Mediterranean area...”.

Things I’m keeping an eye on: Global hunger and humanitarian crisis; debt and currency dynamics in import-reliant countries; growing international efforts to skirt US sanctions and purchase Russian oil and gas exports; renewed calls for serious diplomacy to end the Ukraine war; and, inflation-induced political upheaval in the US and Europe.