March 17, 2023: Global News Roundup

‘Animal spirits’ grip global markets—financial contagion sends central banks scrambling, bond market volatility signals more trouble ahead

This post was originally published on www.IPEwithSBB.org.

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global issues and events.

This was one of those weeks where things happened so quickly that this post may well be outdated before you even have a chance to read it. The financial whirlwind that swept across the globe this week began with last Friday’s collapse of Silicon Valley Bank (SVB) following a bank run. The bank was seized by the Federal Deposit Insurance Corporation (FDIC) on Friday afternoon. Over the weekend, New York-based Signature Bank also failed and was closed by state regulators on Sunday. On Monday, US regulators, including the FDIC and the Federal Reserve, announced emergency measures intended to halt the run on regional banks, guaranteeing depositors’ funds, including substantial deposits over the $250,000 limit that is insured by the FDIC. By Monday, it was clear that contagion was spreading very quickly, and as the week rolled on, investors grew increasingly concerned about Swiss-based Credit Suisse, US-based Charles Schwab, and other US-based regional banks like First Republic Bank (credit rating downgraded to junk on Wednesday). On Wednesday, the Swiss National Bank announced that it would provide emergency liquidity to Credit Suisse if needed.

Stock markets all over the world fluctuated madly as investors tried to discern which banks would fail next and how regulators would respond. I was reminded of John M. Keynes’ comment—"The markets are moved by animal spirits, and not by reason”—referring to the tendency of financial investors to herd, often moving in the marketplace all together (like a herd of livestock) and in seemingly irrational ways. US, European, and Asian stock markets (including in India, Japan, and Hong Kong) fell most of the week, punctuated by short-lived and frenetic periods of investor optimism following announcements of market support measures. Just look at the volatility of the S&P 500 between Monday-Thursday of this week in the chart below. As a good friend remarked to me about financial news this week, “If this were a rollercoaster, everyone would be dead. Or at least incredibly sick.”

(Image: S&P 500 index, 3/13/2023-3/16/2023, courtesy of Trading View, here).

The most unnerving part of this week’s financial news for me was the behavior of markets for US government debt (i.e., Treasuries). Global markets for US Treasuries are the largest and most liquid in the world. US Treasury bonds have for many decades been regarded as a “risk free” asset, and they are the foundation of portfolios all over the world, from retail investors and pension funds to insurance companies, investment banks, sovereign wealth funds, and central banks. Further, futures and options markets on US government debt and US interest rates are expansive and heavily traded globally. In other words, problems in this marketplace mean that contagion is likely to spread far and have an very large impact owing to how widely held these assets are globally (in my forthcoming article for Dollars & Sense, I call this unfolding financial event the Whole World Debt Crisis).

And, boy, problems in Treasury markets multiplied this week. A major underlying reason for SVB’s collapse is that the bank invested depositors’ money in long-term, low-yielding Treasury bonds. As interest rates rose over the past year, these low-yielding bonds lost value, because investors grew interested in buying higher yielding bonds issued more recently at higher rates. SVB thus had “unrealized losses” on its portfolio (“unrealized” because SVB hadn’t sold them yet, so the losses hadn’t been “booked”). As the bank run proceeded and depositors withdrew funds, SVB had to sell those long-dated Treasuries at a loss, turning an unrealized loss into a realized loss that showed on the books. These losses further reduced depositor and investor confidence, which resulted in more withdrawals and plummeting share prices. As other banks and financial firms saw what was happening, they panicked and rushed to cover their own positions, so as not to get caught in the same bind as SVB. As Fortune India noted on Monday, “Banks in the US are sitting on a record cumulative loss of $620 billion on their bond portfolio.” Seemingly overnight, the market for US Treasuries became wildly imbalanced.

Further complicating matters was the US government intervention to bail out the struggling banks, which investors interpreted to mean that the Federal Reserve would likely decide to halt rate hikes and start up quantitative easing again. So, on top of the pressure from the SVB collapse, interest rate expectations also fluctuated dramatically over the course of the week. The turbulence in bond markets resulted in lower liquidity and a trading halt in US interest rate futures markets on Wednesday (in the SOFR futures market—Secure Overnight Financing Rate—in which banks and other big investors speculate and hedge risk on future US interest rate movements). The Financial Times quoted a portfolio manager on this week’s liquidity issues: “We’re doing trades of any size on the phone and negotiating prices more carefully. Going to the screens to execute electronically is painful.” Bid-ask spreads are rising, and one trader quoted by Reuters on Monday estimated that the spread is “three to four times wider than normal” and that the “ability to trade in and out of positions is ‘definitely worse than the Ukraine war’”, referring to sharp declines in market liquidity last year when Russia invaded Ukraine.

Moreover, the new trouble in US government bond markets, stemming from the SVB collapse and the response from regulators, is occurring in a context in which US government debt was already beginning to worry investors. Two days before the SVB crash, FT reported that the cost of default insurance on US government bonds (called credit default swaps, or CDS) had risen eight-fold, from 10 basis points at the beginning of the year to 80 points as of March 8, 2023, largely owing to the US having hit its debt ceiling in mid-January (there is no agreement yet in the US Congress about raising the ceiling). By Monday March 13, following the SVB and Signature bank collapses, the cost of insuring against a US government default had risen by another roughly 11% to just under 90 basis points.

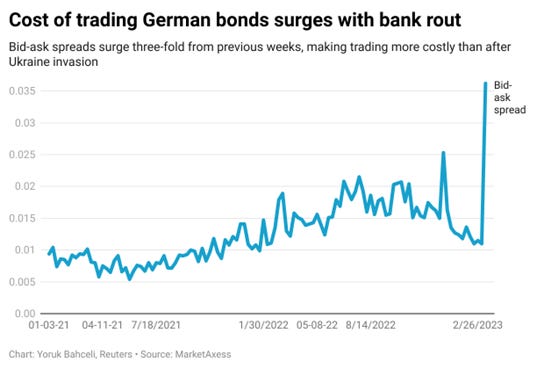

And it wasn’t just the market for US government bonds. The German government bond market also struggled with widening spreads and decreasing liquidity this week. (When the bid-ask spread is zero, the trade is said to be “frictionless” or without cost, and the market tends to be highly liquid because it’s easy to agree on a price and make trades happen. Conversely, the higher the spread, the more expensive the trade, so fewer trades are made.) The chart below from Reuters shows the increasing cost of trading German bonds over the past two years, with the spread exploding since the SVB collapse.

(Image: Cost of trading German bonds surges with bank rout, from Reuters, here).

Like SVB and apparently most other banks, the German central bank (the Bundesbank) has been struggling since last year with losses on its asset portfolio stemming from the declining value of government bonds: “The Bundesbank has suffered a €1bn hit from its substantial bond holdings and warned future losses would wipe out its remaining financial buffers as the German central bank grapples with the impact of higher interest rates…The Bundesbank has bought €1tn of mostly German government debt since 2015 as part of the European Central Bank’s bond-buying programmes…,” reported the Financial Times on March 1, the week before SVB collapsed. This is the much the same situation in which the US Federal Reserve finds itself because the US Federal Reserve system is the single largest holder of US government debt (the Fed owns close to 20% of US government bonds). By September 2022, the Federal Reserve system had almost US$690 billion in unrealized losses associated with its investments in Treasury securities.

This suggests that the global financial system’s largest institutions, the public ones that are supposed to act as lenders of last resort in times of crisis, are themselves struggling with the very same problems that they are currently trying to fix in the private banking sector. For the Bundesbank, the losses they’ve taken over the past year mean that there is almost no “buffer” left, as higher deposit rates and lower returns on its investments squeeze its margin. The losses they took last year were paid for with buffer funds set aside in prior years, buffers that are rapidly depleting. I’m deeply concerned that government bond market problems combined with fragile central bank balance sheets indicate an incoming financial event much larger, more serious, and more difficult to contain than a mere banking crisis.

In other, totally unrelated news about real animal spirits, a two-year old kid in Australia chased a snake across the front yard this week and discovered a nest containing over 100 snake eggs. They were Eastern Brown snakes, the second most venomous land snake in the world. Fossils of “the earliest-known ichthyosaur” dated 250 million years ago were discovered in an Arctic region of Norway. Ichthyosaurs are a marine reptiles some of which grew to 70-feet long! And, last, I’m saddened that the Straits Times reported this week that the French bulldog has replaced the Labrador retriever as the most popular dog in the United States. Labs rock. (No offense to Frenchie-lovers).

Things I’m keeping an eye on:

1. Interest rates and market support: On Thursday morning, the European Central Bank hiked interest rates again, by 50 basis points. Will the Fed follow? This could seriously upend investor expectations and further roil bond markets. Also interesting, on Thursday some of the US’s largest banks announced a $30 billion plan to rescue First Republic Bank: “The actions of America’s largest banks reflect their confidence in the country’s banking system. Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most,” wrote Bank of America, Citigroup, JP Morgan Chase, Wells Fargo, Morgan Stanley, BNY-Mellon, BNC Bank, State Street, Truist, and US Bank. They must be really worried.

2. Ukraine war: Great Powers flirted with direct military confrontation this week, with the US and Russia trying to manage a dispute around a downed US surveillance drone that had some kind of confrontation with a Russian fighter jet in disputed airspace over the Black Sea. Each side is accusing the other of escalating the war, and recently released video shows the Russian jet intercepting the drone. Thankfully, US and Russian officials are actually talking to one another about the incident in an attempt to cool tensions.

3. Global economic conditions: This week, Argentina’s annual inflation rate surpassed 100%. Korea recorded its largest monthly current account deficit since they started collecting data in 1980. China is increasingly concerned about large local government debts, and workers in the UK went on strike to address falling real wages and deteriorating standards of living.

4. The emerging military-economic blocs I wrote about last month are solidifying quickly. The AUKUS alliance (Australia-UK-US) agreed this week on a deal to share nuclear submarine technologies. Meanwhile, China brokered an agreement between Iran and Saudi Arabia, paving the way for future collaboration and utterly disrupting US foreign policy in the Middle East. Honduras also switched its recognition from Taiwan to China this week, opening up diplomatic relations with the mainland.

Thank you for reading and supporting my work! I am taking a couple of weeks off from the Substack and will be back with a new post on Friday April 7.

Thank you so much for reading!!! And for taking the time to comment!

Fantastic article.

Now I can't wait for April 7th for the next post!