May 19, 2023: Global News Roundup

May 19, 2023: Global News Roundup

The global debt crisis continues—an update

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global issues and events.

I’ve written a lot about debt here on Substack over the past year, including articles from June, August, and two in January (here and here), as well as my March cover story for Dollars & Sense on what I call the Whole World Debt Crisis. Today’s post is an update on the global debt situation, with particular focus on sovereign (i.e., government) debts.

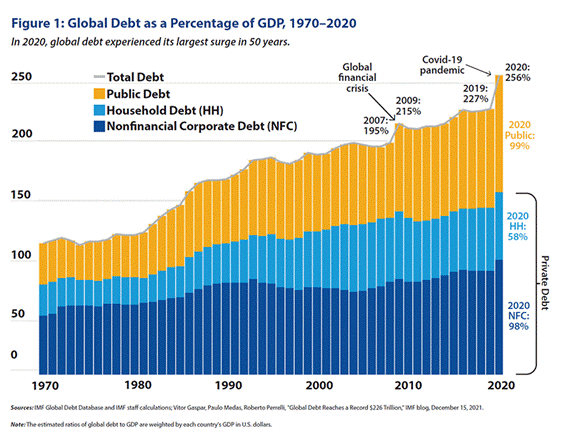

Beginning with the general global debt terrain, the chart below illustrates the situation between 1970-2020, with government, corporate, and household debts all steadily climbing over this period as a percent of GDP. The pandemic and its associated supply chain disruptions, followed by the Ukraine war and rising US interest rates, conspired to drive up debt levels even further in the several years following.

(Image: “Global Debt as a % of GDP, 1970-2020”, from “The Whole World Debt Crisis” by Sasha Breger Bush, Dollars & Sense, Mar/Apr 2023, here).

It was reported this week that global debt levels continue to skyrocket, including in emerging markets: “Emerging market debt has hit a record high of over $100tn, a third higher than pre-pandemic levels…Global debt rose by $8.3tn in the first three months of the year to $306.3tn, the highest level since the first quarter of last year and second-highest quarterly reading ever…Global debt is now $45tn higher than its pre-pandemic level and is “expected to continue increasing rapidly”, noted the Financial Times citing a report from the Institute of International Finance.

Turning to Sudan and Pakistan, ongoing civil conflict is aggravating debt problems and casting a negative light on the power of the International Monetary Fund (IMF, or the Fund), an international organization based in Washington DC charged with ensuring international monetary and financial stability. An op-ed in New Age (out of Bangladesh) this week explained how decades of IMF structural adjustment policies prior to the recent conflict—policies which require debtor states to undertake economic reforms as a condition of receiving emergency loans—hollowed out the Sudanese economy, undermined food production, permitted predatory foreign investment, undermined the ability of the government to meet the needs of residents, and empowered the military leaders central to the conflict raging today:

The IMF also dealt with Sudan harshly, cutting off credits and aid at the slightest sign of non-compliance or policy disagreement and imposing increasingly severe terms. The dynamic was so perplexing that scholars used Sudan as a case study to understand power struggles in IMF programs… Since October 2021, the Sudanese people have protested the military takeover at the cost of hundreds of lives. On the surface, the ‘international community’ seemed to punish the military coup by suspending aid and debt relief, but on the ground, the military regime was given a seat at the negotiating table and perhaps even a position of priority in dictating the ‘peace terms.’

Sudan qualified for debt relief via the IMF and World Bank’s Heavily Indebted Poor Countries Initiative (HIPC) back in 2021, before the recent conflict erupted, following decades of “isolation from the international financial system”. The Al-Monitor reported last month that the IMF “projects Sudan’s economy to retract this year by 2.5%, the worst of all states surveyed in the Middle East and Central Asia (MECA). Inflation is expected to be 71.6% and unemployment 32%, also the worst in the region. About a third of the population lives below the international poverty line of $2.15 per day, and close to 70% below the middle income poverty line of $3.65 per day, according to the World Bank.”

Turning to Pakistan, where an economic crisis has been raging since last year and the rupee fell 50% relative to the US dollar over this period, the government is rapidly depleting its foreign exchange reserves, with only enough remaining to cover about a month of imports. Pakistan’s existing agreement with the IMF expires in June, and negotiations to renew it have stalled. “A staff-level agreement on the review has been delayed since November, with nearly 100 days passed since the last staff level mission to Pakistan - the longest such delay since at least 2008”, reported Reuters this week. Ongoing civil unrest related to the arrest of former President Imran Khan is casting more doubt on the debt deal according to analysts: “The latest developments likely dampen any prospect of a political breakthrough…”. Last week Pakistani Finance Minister Ishaq Dar tried to soothe global investors while also affirming the country’s stance on the IMF’s demands for policy reform, noting “that Pakistan would not default, with or without the IMF, and that the country could not afford to take any additional harsh measures to accommodate the IMF.”

But Sudan and Pakistan sure aren’t alone. Because the world has a lot of countries (195, at last count) and so many of them are struggling with unsustainable debts at the moment, I do not have space to provide detail on all relevant cases. Here are bulleted highlights from as many other cases as I could fit in before Substack told me that this email was too long to send to you.

· Sri Lanka. Sri Lanka defaulted on its debts in April 2022, with protests and riots over the deteriorating economy and rising prices of essentials like food and energy ultimately succeeding in ousting President Rajapaksa by July. Before he left office, Rajapaska began negotiations with the IMF for an emergency loan. The negotiation and debt restructuring process is still ongoing now, some 13 months later, though it appears that some progress has been made and a deal might be finalized by September. According to Mena FN, “Sri Lanka owes $7.1 billion to its creditors, the latest government data shows, with $3 billion owed to China, $1.6 billion to India and $2.4 billion to the Paris Club, a group of major [mostly Western] creditor nations.” Among other obstacles, China has been reluctant to participate in debt restructuring talks and the IMF is requiring substantial and difficult reforms of Sri Lanka as a condition of the loan package, including fiscal austerity and anti-corruption measures.

· Egypt. Egypt’s economy has been in crisis since last year: “Egypt’s national debt has been ballooning — $224.79 billion in 2022, up from $193.94 billion the previous year. The Ukraine war sent inflation sky-high and increased the cost of importing essential grains and fertilizers, causing foreign investors to flee and the Egyptian pound to tank by around 50% against the US dollar.” The IMF extended a US$3 billion loan package in December, but it hasn’t been enough to stave off the prospect of default. Egyptian President Abdel Fattah al-Sisi has downplayed the default risk, and has refused to implement some of the reforms required by the Fund to secure additional financing. Among other demands, the IMF wants the government to liquidate its holdings in state-owned firms, a kind of partial privatization. While the government initially refused, this week al-Sisi’s government announced it was selling a minority (9.5%) stake in state-owned Telecom Egypt. Egypt is also likely to receive financial support from various Gulf states, like the UAE and Saudi Arabia, with a vested interest in supporting regional economic stability.

· South Africa. Following February’s declaration of a national state of emergency owing to serious trouble in the energy sector including frequent blackouts and mass protests, South African Finance Minister Enoch Godgonwana provided a “bleak” update this week, noting low growth prospects (South African GDP contracted by 1.3% in 4Q 2022) and fiscal pressures that would be difficult to address. Like many other debtor states, South Africa’s economic crisis is deeply intertwined with the Ukraine war—the war has driven energy and food price inflation and South Africa was also recently accused by the US of supplying weapons to Russia which precipitated a rapid depreciation of the local currency (the rand) to an all-time low.

· Zambia. Zambia inaugurated the Whole World Debt Crisis when the government defaulted on a Eurobond payment back in November 2020. “In early 2021, Zambia agreed to be a guinea pig for a new approach to tackle sovereign debt — the G20 Common Framework for Debt Treatment, introduced at the end of 2020”, according to the Mail & Guardian (out of South Africa). The idea with this initiative was to create a framework to bring all creditors together to negotiate debt restructuring, not only the so-called “Paris Club” of Western government creditors, but also private creditors and other non-Western governments like China and India. But there has been little progress to date, because the IMF has not succeeded in bringing all the relevant creditors to the table: “And this is the problem Zambia is facing. A chunk of its debt is owed to private creditors, and not all parties will cooperate. Without a deal, it cannot unlock the promised IMF-support reform programme of $1.4 billion. It also cannot untangle itself from the framework.” Meanwhile, Socialist Party President and award-winning journalist Dr. Fred M’membe is rallying support for different kinds of reforms, ones that would support domestic food production and peasant agricultural production, explicitly in opposition to the IMF’s mandates, which he deems “financial colonialism”: “The IMF deal that this government has pressed its entire hope on will not help us much to address the country’s rocketing prices, growing poverty, desperation, and joblessness,” said M’membe earlier this month.

· Ghana. My prior article for D&S from March covered Ghana’s case in more depth, so I’ll keep this short here. Part of the issue with securing an IMF deal up to this point was wrangling creditors and working out some sort of debt deal both with private bondholders and sovereign creditors like China. Just this week, the IMF finally approved the US$3 billion loan deal, with US$600 million for immediate release. The ability of Ghana to negotiate the demands of so many different creditors—a problem that Zambia and Sri Lanka and others are also facing—is quite a feat and may help other nations find a way out of their own debt crises.

· United States. As I’ve mentioned in prior articles, it’s not only so-called “developing” economies that are struggling with massive debts. The United States is slated to reach its “X-date”, the date beyond which the Treasury will have to start deciding what not to fund (debt service, wages for government employees, or social programs, etc.), as soon as June 1. Negotiations are ongoing and no deal to raise the debt ceiling has been reached at this time. Credit default swap prices for US government debt (CDSs, financial securities that provide a kind of insurance against US government default) reached record highs this month. On Thursday, Democratic members of the US Congress wrote to President Biden to ask him to use the 14th Amendment to override their Republican opposition should debt negotiations fail. “We write to urgently request that you prepare to exercise your authority under the 14th Amendment of the Constitution, which clearly states: ‘the validity of the public debt of the United States…shall not be questioned,'" read the letter. While a deal may still be struck any moment, “Banks, brokers and trading platforms are prepping for disruption to the Treasury market, as well as broader volatility.”

Things I’m keeping an eye on:

1. Peace! This was an excellent week for peace. On Tuesday, the President of South Africa announced a six-nation peace mission to Europe to meet with Russian President Putin and Ukrainian President Zelensky, including South Africa, Senegal, Uganda, Zambia, Egypt, and the Republic of Congo. On Wednesday, FT reported that members of the G7 are preparing to discuss a Ukraine peace summit at the G7 summit in Hiroshima, Japan that begins next week. On Thursday, a suggestion from the US to “freeze” the Ukraine conflict made the rounds in international news, with US officials likening this possible outcome to the situation with North and South Korea, in which the conflict is no longer “hot” but no formal peace has been made. Ukraine Today noted that a freeze or some kind of cessation of hostilities is “becoming increasingly likely amid a growing sense in the [Biden] administration that the upcoming Ukrainian counteroffensive will not inflict Russia a fatal blow”. This is an important admission, coming as the US and its allies in Europe encounter growing obstacles to victory and seek to pivot out of the conflict. Chinese envoy Li Hui was also in Europe this week to speak with President Zelensky and other heads of state about the possibility of a peace settlement.

2. Black Sea Grain Deal: This week, the deal was extended for another 2 months! Great news for global food prices, which had fallen below pre-war levels earlier this year but started to rise again last month.

3. The US economy: Not only is the financial system in very deep trouble (debt ceiling, Treasury markets, banking, commercial real estate, etc.), but ordinary American households are really struggling, indicating that, while a recession has yet to be officially declared, we are already knee-deep in a nasty one. Just as one example, reports over the past month indicate that hunger and food insecurity are back up to pandemic-era levels in the US even as official unemployment levels remain low by historical standards (see, e.g., here). US household debt also hit a record $17 trillion this week: “The figure reveals the enormous financial stress on working class families. Rapidly rising prices for gasoline, food, rent and other basic necessities have devastated household budgets, forcing working people to borrow on their credit cards or take equity out of refinancing their homes to pay their bills.”

4. The UK economy: I could have included the UK in the debt discussion above, but this is a long post as it is. I’m keeping my eye on the UK bond market (they call their bonds “gilts”) and on rising food and financial insecurity among households.