November 25, 2022: Global News Roundup

WTO and IMF sound alarm as deglobalization intensifies

This post was originally published on IPEwithSBB.org.

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global issues and events.

Two publications released last week by prominent international organizations warned about global economic fragmentation. What’s interesting about them is not the pro-globalization positions taken by the World Trade Organization (WTO) and International Monetary Fund (IMF)—both of which have strongly advocated for open global trade and other pro-globalization policies for decades—it’s the data presented about how the global macroeconomic landscape has changed over the past several years. I highlight some of the key facts below, with a bit of context and discussion.

The first publication is the text of a speech, entitled “Overcoming Fragmentation: ‘Stay Open, Connected and Balanced’”, delivered by IMF Managing Director Kristalina Georgieva at the APEC Leaders’ Summit in Bangkok, Thailand on November 19 (APEC = Asia Pacific Economic Cooperation):

· “The pandemic has caused a permanent loss of economic output equal to 5.3% of global GDP. In Asia--a very integrated region--this was even higher, a loss of 9% of GDP.”

Note that income losses were higher in more “integrated” regions, i.e., those areas of the world that depend more heavily on open global markets bore higher costs as trade was restricted.

· “In addition, the war in Ukraine caused a tremendous energy price shock.

The combined impact of these two events [pandemic and Ukraine war] was an abrupt slowdown of global growth from 6.1% in 2021 to 3.1% in 2022.”

· “APEC in particular has greatly benefitted from integration--that is 21 economies representing 60% of global GDP. Asia has the strongest regional value chains; Latin America's biggest trading partners are across the Pacific; two-thirds of U.S. imports comes from APEC.”

· “IMF analysis indicates that, if the world were to divide into two distinct blocs with little or no trade between them, output would drop by more than 1.5% of global GDP: a loss of about $1.5 trillion. In Asia, because it is so integrated, these losses would double to more than 3 percent of GDP.”

These estimates—which seem pretty modest, and I’ve certainly seen more ominous ones—are clearly rooted in concerns about the consequences of growing economic conflict between the US and China. In this context, the speech also seems to be a veiled critique of contemporary US and Chinese economic policies that increasingly focus on economic warfare and “decoupling”.

· “The IMF is projecting global growth to slip to 2.7% next year. Most APEC countries are decelerating and at least one third of the world is going to be in recession.”

The second publication is a report on “G20 Trade Measures” from the WTO released on November 14. General findings on trade protections and global growth include:

· “Since 2020, the pace of implementation of new [trade] restrictions by WTO Members, in particular on the export side, has increased, first in the context of the pandemic and more recently in the context of the war in Ukraine and the food security crisis. WTO Members have gradually lifted some of these export restrictions. As of mid-October 2022, 52 export restrictions on food, feed and fertilizers and 27 COVID-19-related export restrictions on essential products to combat the spread of the virus were still in place. Of these, 44% of export restrictions on food, feed, and fertilizers and 63% of pandemic-related export restrictions were maintained by G20 economies (p. 3).”

Market interventions to ensure regular food supplies and stable food prices are, historically, very common national policy responses to food crises and food price volatility, including in other recent food crises in 2007-2008 and again in 2011-2012. But these particular restrictions noted by the WTO in this report—on food, fertilizer, and covid-related supplies—have a nasty regressive effect in that they are restrictions mostly imposed by wealthier countries on basic necessities that are in short supply in poorer countries, where the population already bears a disproportionately high burden from rising food prices.

· It is thus unsurprising that: “The majority of the trade concerns raised in WTO bodies concerned G20 measures or policies (p. 3).”

One major role for the WTO is to serve as a forum for the resolution of international disputes over trade. The WTO notes in this recent report that most of the concerns it is hearing from members are about the restrictions that G20 countries—which include the largest and wealthiest economies in the world—put in place and have kept in place since the pandemic began. As noted above, some of these restrictions are in agriculture and work to reduce food and fertilizer exports, thereby increasing prices on the global market.

· “The medium-term outlook for trade has deteriorated after a series of related shocks hit the global economy during the review period, prompting the WTO to downgrade its projections for the next 18 months. Merchandise trade is now expected to slow in the second half of 2022 and to remain subdued in 2023 as the war in Ukraine, high inflation, and lingering side-effects from the COVID-19 pandemic weigh on global economic growth. The WTO expects world merchandise trade volume growth of 3.5% in 2022 (up slightly from the previous estimate of 3.0%) followed by a 1.0% increase in 2023 (down sharply from 3.4% previously) (p. 7).”

· Elaborating on severe global commodity price inflation, the WTO notes: “Energy prices in September were up 47% year-on-year and 125% compared to January 2021. The increase was led by natural gas, prices of which rose 118% year-on-year and 433% since January 2021. The 19% year-on-year increase in the price of crude oil in September is small compared to rise in natural gas, but it is still significant for consumers. Crude oil prices remain high, having risen 64% since January 2021 (p. 8). The chart below depicts commodity price increases since 2019:

(Source: WTO report on “G20 Trade Measures”, Chart 2.2, p. 8, in the original here).

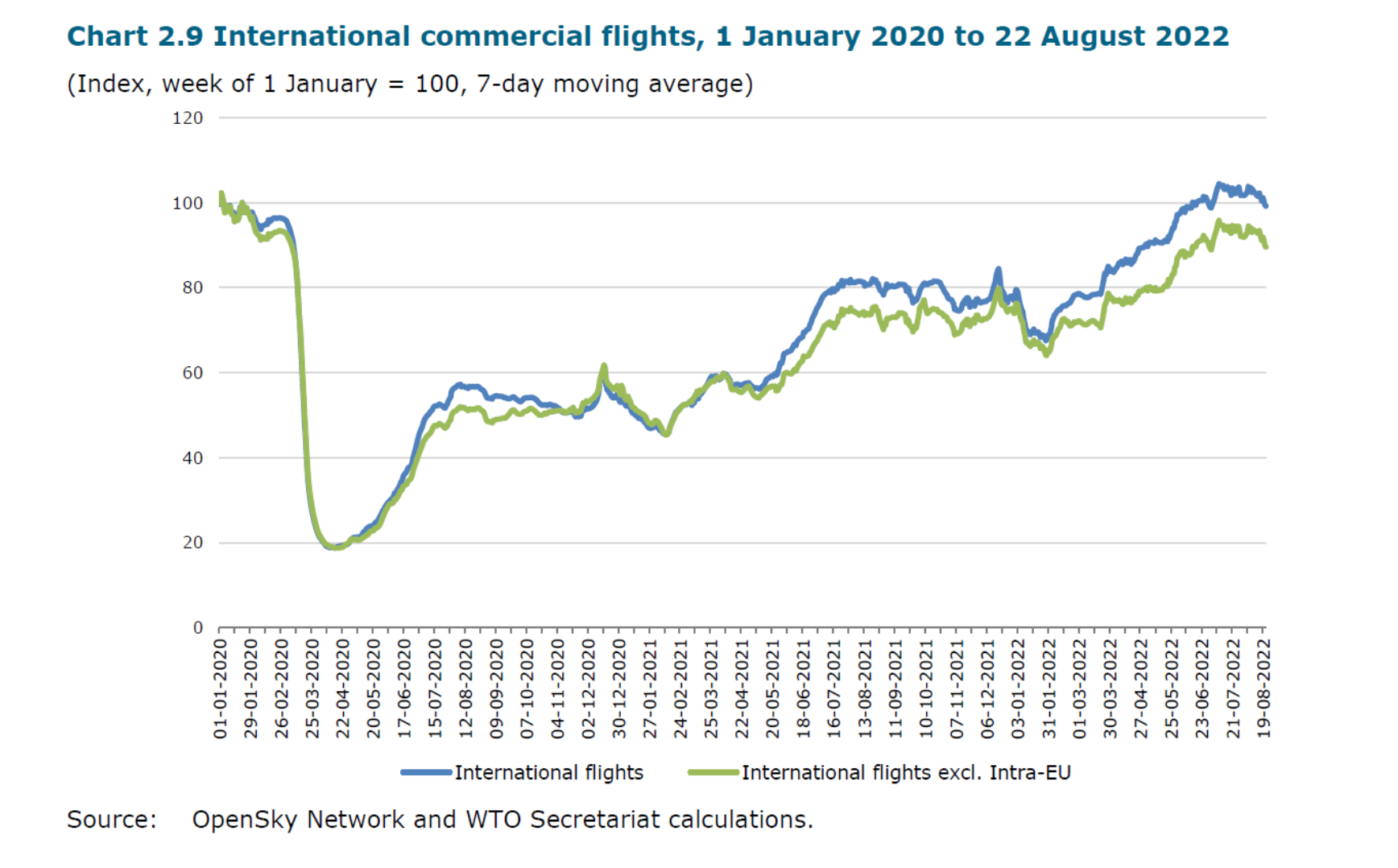

The report is chock full of interesting stuff about economic integration and disintegration, and I’ll share just one more chart, below, of international commercial flights between January 2020 and August 2022. International flights (which include business, tourism, and diplomatic travel) have only just recently recovered to pre-pandemic levels.

(Source: WTO report on “G20 Trade Measures”, Chart 2.9, p. 14, in the original here).

When the WTO report was released right before the G20 meetings last week, WTO Director-General Ngozi Okonjo-Iweala pressured G20 governments to conduct policy in ways that do not so harshly penalize emerging economies struggling with dire food and energy crises: “Export restrictions contribute to shortages, price volatility, and uncertainty. G20 economies must build on their collective pledges from the 12th Ministerial Conference and demonstrate leadership to keep markets open and predictable, so that food and fertilizer in particular can flow to where they are needed.”

Things I’m keeping an eye on:

1. Deglobalization dynamics: Not just trade protection, but also other forms, such as capital controls (are we approaching suspensions of convertibility as the dollar soars and capital flight bites?) and more restrictive immigration policies (e.g., Italy).

2. Election mayhem: Malaysia, Brazil, US (Arizona).

3. The gold “whales”: Last week I was keeping an eye on large sovereign gold purchases by unidentified governments. This week news broke that this is probably China stockpiling gold to reduce dollar dependence. De-dollarization is another facet of deglobalization; as the global economy fragments, global demand for dollars falls.

4. Knock-on effects from the FTX collapse. I don’t think this story is over yet.

5. Possibility of a national rail workers strike in the US starting in December.

6. The World Cup! The BBC and Al Jazeera both have live updates running on their homepages.