October 21, 2022: Global News Roundup

Chip War intensifies as Xi charts bold path for China

The Global News Roundup collects news stories from entirely international (non-US) media sources on variety of pressing global political and economic issues and events.

General Secretary of the Chinese Communist Party Xi Jinping opened the 20th CCP National Congress this past Sunday with a speech, one many analysts believe indicates a significant change in China’s international outlook and strategy. Among other important comments, Xi remarked, “We must meet obstacles and difficulties head on, ensure both development and security, and dig deep to surmount the difficulties and challenges on the road ahead. Let us harness our indomitable fighting spirit to open up new horizons for our cause.” He specifically addressed Taiwan: “We will continue to strive for peaceful reunification with the greatest sincerity and the utmost effort, but we will never promise to renounce the use of force, and we reserve the option of taking all measures necessary.” This link takes you to a video about this year’s National Congress prepared by the Chinese government for foreign journalists. Note especially the effort to project global power and influence, not merely regional power.

Taiwan responded quickly and forcefully. “Taiwan will not back down on its sovereignty or compromise on freedom and democracy,” said the Office of the President of Taiwan on Monday. “Beijing is pursuing its plans to annex Taiwan on a “much faster timeline” under Chinese President Xi Jinping”, said US Secretary of State Anthony Blinken, also on Monday. On Wednesday, the South China Morning Post reported that “China’s top military brass have vowed to be on high alert and prepared for war as the nation faces mounting military confrontation with the United States.” And a top US Navy official said “on Wednesday that a mainland Chinese invasion of Taiwan could take place as soon as this year…”.

(Image: Episode from the Four Days' Naval Battle (11-14 June 1666) by Willem van de Velde (I), painted between 1666-1672, depicting a naval battle during the Second Anglo-Dutch War. This series of wars over trade and colonial territories began in 1652, shortly after the British passed the 1651 Navigation Act, which prevented Dutch ships from carrying cargo into British-controlled ports. Image courtesy of the Rijksmuseum, here. A write up on the vicious 4-day battle from the US Naval Institute can be found here.)

Lurking behind the heated official rhetoric is the raging US-China economic war, especially the conflict over semiconductors. Indeed, recent events suggest that it’s China’s huge new computer chip problem that may ultimately determine the timing of any move against Taiwan. On October 7, the US announced new semiconductor export controls. The controls prevent China from using American semiconductor technology and expertise, inhibiting China’s ability to import and produce cutting-edge chips used in a variety of sectors deemed critical to its national security and future economic growth. According to virtually every account I’ve read, this particular set of export controls is already doing substantial damage to both US and Chinese chip manufacturing, with broader knock-on effects expected for their already-struggling economies (see here, here, here, here, here, and here for a variety of perspectives on the new controls and broader Chip War).

In an op-ed in the UK’s Financial Times on Wednesday, Edward Luce discussed the political and military implications of the controls: “There are two big risks to Biden’s gamble. The first is that America is now close to making regime change in China its implicit goal… The [second] more imminent risk is that Biden’s gamble could prompt Xi Jinping, China’s president, to accelerate his timetable for Taiwan reunification. The island state is by far the world’s largest maker of high-end chips”.

Along similar lines, AsiaTimes ran an interesting article last year that discussed Taiwan and computer chips in the broader context of China’s goals and capabilities:

But consider the upside from a Chinese perspective:

Seize control of Taiwan and you’ve upended the US defense posture in the Indo-Pacific. The PLA will have broken the so-called First Island Chain stretching from Japan to Malaysia, which hems in Chinese forces.

And with a lodgment in the center of the US and allied defense line, the PLA can extend its reach outward and drive a salient into the heart of America’s central Pacific defenses.

Meanwhile, lines of communication between Japan and Australia are threatened, and a PRC-occupied Taiwan eliminates a launch point for attack and intelligence collection against the Chinese mainland. It could also give China access to Taiwan’s strategic chip manufacturing.

For a Chinese defense planner, Taiwan is worth a very high price. It would also give Beijing massive psychological and political advantages. Take Taiwan and you demolish American prestige in the region and globally.

The Malaysia Sun reported this week on China’s response to the new chip controls: “China Saturday criticized the latest U.S. decision to tighten export controls that would make it harder for China to obtain and manufacture advanced computing chips, calling it a violation of international economic and trade rules that will "isolate and backfire" on the U.S.” Xi himself has “vowed victory” against the US: “We will accelerate the realization of a high level of technological self-sufficiency,” said Xi on Sunday, according to the Straits Times. It appears that the chip problem has the potential to change China’s cost-benefit calculus regarding a blockade or invasion of Taiwan.

In a related vein, Singapore’s Prime Minister Lee Hsien Loong shared some rather ominous-sounding concerns this week about how rapid US-China economic “decoupling” will impact the rest of the world (decoupling means separating the two tightly intertwined economies, reducing interdependence; the US export controls are an example of a policy geared toward decoupling): "We will have to see how things work out, but we do worry that valid national security considerations may trigger further consequences and may result in less economic cooperation, less interdependency, less trust and possibly ultimately a less stable world.”

There were also warnings from China this week, the general message being that the US and EU risk their own economic welfare and that of other countries by limiting trade and investment with China. Chinese state media ran several pieces this week with this theme, one about US aircraft manufacturer Boeing’s reliance on the Chinese market, another about Europe’s reliance on the Chinese market, and still another about the dangers of the US chip strategy for global stability. “Shortsighted Washington is still dreaming of advancing its interests through "decoupling" from China. But its allies and partners seem to have understood the deep-seated and long-term dangers of "decoupling" better than the US itself”, stated the Global Times, a CCP-run media outlet. Critically, the article also quotes German Chancellor Olaf Scholz warning about the dangers of deglobalization and decoupling from China. Within the broader context laid out above, it’s hard not to see such statements from official Chinese state sources as working to create a pretext within which to oppose possible US sanctions or other punitive economic measures in the future.

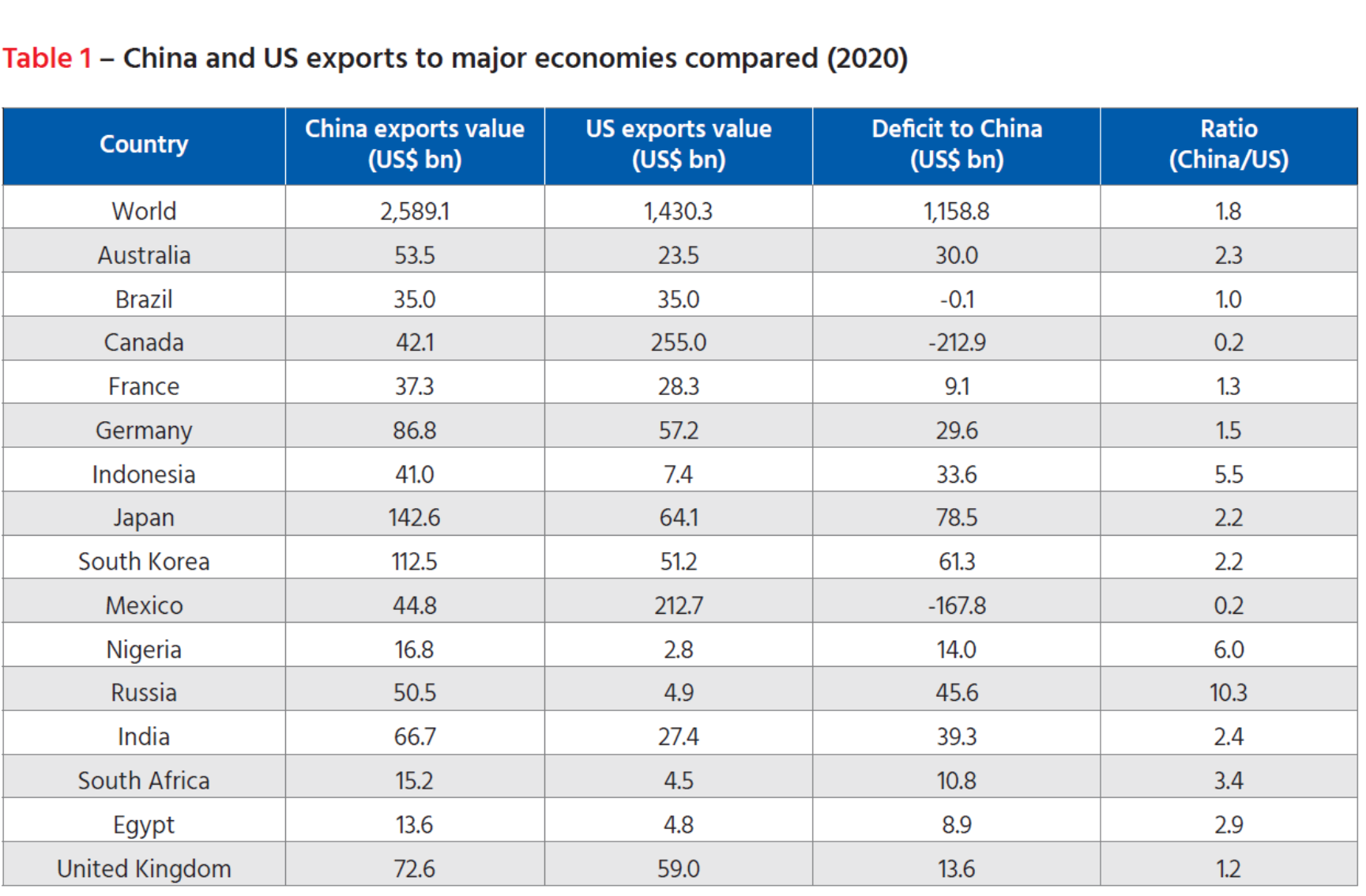

The cost of compliance with sanctions or other similar measures, should they been enacted by the US and its allies on China moving forward, will generally be significantly higher for most countries than it is currently with Russia. Dependence on Russian oil and natgas notwithstanding, most of the world’s countries rely much more heavily on China’s economy than Russia’s, and China will surely continue to fully exploit their dependence to its advantage as the situation continues to escalate. The Hinrich Foundation, an international nonprofit, published a report last month that tackled exactly this question, i.e., “the degree to which the world economy has become dependent on China and the implication this has for the ability and willingness of countries to stand up to China when their interests diverge”. The table below shows Chinese versus US exports to other major economies, with a ratio of the value of Chinese to US exports in the far-right column. The author concludes as follows: “Outside this American affair [Canada and Mexico], though, it is a very different story, particularly in the global south. Out of 229 jurisdictions in the Comtrade database (excluding mainland China and the US), China is the larger exporter to 173 of them, while the US is the larger exporter to 56… Even America’s closest security allies such as the UK, Australia, and Japan now import more from China than they do from the US.” China is also a primary destination for the global south’s exports, as well as a central participant in international financial markets.

(Source: “How Dependent Has the World Become on Trade with China? Does it Matter?” by Stewart Patterson. Hinrich Foundation, September 2022. Original report here.)

Things I’m keeping an eye on:

1. British political instability. UK Prime Minister Liz Truss resigned on Thursday after a few weeks of trying futilely to dig herself out of the economic hole she and her cabinet dug themselves last month. She is the shortest serving Prime Minister in British history (44 days).

2. Saudi Arabia: In response to the OPEC+ production cuts two weeks ago, US lawmakers are again floating the NOPEC legislation, which aims to undermine the OPEC oil cartel by allowing US entities to sue OPEC members for antitrust violations. Given the obvious dangers—including that Saudi Arabia already recently defied the US and could dump the petrodollar if NOPEC passes—I’m curious if the US will proceed. There is already significant enthusiasm among BRICS countries about undermining global dollar supremacy, and there was confirmation this week that Saudi Arabia’s does indeed plan to join the BRICS organization.

3. Margin calls, emptying metals vaults. With recent market volatility and shrinking liquidity, I have to think there are gigantic margin debts lurking beneath the surface. We got a taste of this a few months back with European energy derivatives markets, and also more recently with UK pension fund interest rate swap deals going sideways (see last week’s post). On a similar note, I’m curious about what’s going to happen with the quickly decreasing stocks of deliverable metals on the London Metal Exchange (and maybe other exchanges too?). Check out this recent article on low lead stocks, and this one on the LME’s predicament regarding metals sourced from Russia (e.g. copper), as well as this one on LME’s low “shadow” stocks from back in April which noted that “the evaporation of this buffer stock means any call on metal from the market of last resort must be made on the dwindling volume of registered inventory.”